Scrap the Cap: Everyone Should Retire Healthy and Wealthy

A column on the first step toward universal income — fixing the insurance we already own.

The road to universal income is long, and I’d rather talk about the first step than the horizon, because the first step is already paid for. We built the machine generations ago. We funded it. We trust it. It’s Social Security, and right now it runs with a flaw in its spine. Correct the flaw and you’ve taken the first real step toward a country where growing old never means growing afraid.

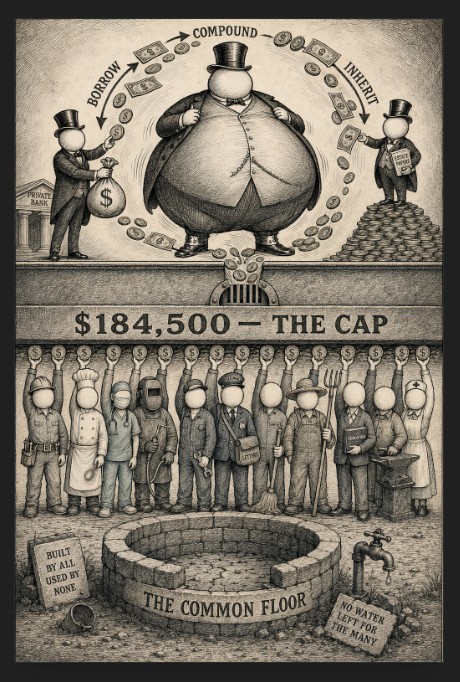

The flaw has a number. In 2026 it’s $184,500.- A wage that fewer than 6% of Americans EVER earn.

When people say scrap the cap, they picture a billionaire, and the billionaire is the wrong man to picture. Social Security taxes wages. The billionaire’s fortune sits in capital gains, dividends, and stock he borrows against and never sells. The cap never reached him. He was never standing in the line you want to close.

The cap reaches someone else. Every dollar earned up to $184,500 carries the 6.2 percent Social Security tax. The dollar after it carries zero. So the person sitting right at the cap pays the most anyone in America pays — $11,439, the full rate on every dollar he earns. He’s the last full member of the common project. Cross that line by a dollar and the rules change for the rest of your climb. By half a million in wages, the effective Social Security rate has fallen to 2.29 percent, about a third of what the dishwasher pays on every dollar she makes.

That line is a seam. It’s where a wage stops behaving like a wage and starts behaving like capital. Below it your dollars get spent — rent, food, the car that gets you to the job. Above it your dollars get invested, and invested dollars compound, get borrowed against, and get handed down. The whole machinery by which money makes more money and passes to your children sits above that line, and Social Security has agreed not to cross it.

Here’s the small number and the large one in the same breath. For someone just over the cap — a $200,000 earner — the slice the cap shelters comes to about $961 a year. You’d never feel it leave. Invest that $961 a year across a working life and it grows to roughly $192,000. Hand it to a child and let it sit another twenty-five years and it becomes about a million dollars. A seven-figure head start, grown from an amount the earner couldn’t have told you was missing. That’s how aristocracies actually get built. Seams like that one do the work the yachts only advertise.

And it’s a small class to begin with. About one working American in twenty-eight ever earns enough to reach the cap. Stack the sheltered surplus on top of who gets the internship, the referral, the seat that opens because someone’s father made a call, and you have a hereditary capital class that clocks in at nine and calls itself earned.

Insurance held in common works one way: everyone pays the same rate in, and everyone draws the same out. We broke both halves. We cap what the comfortable pay, and we scale what people draw by what they once earned, so the program ends up mirroring the very inequality it was built to insure against. There’s an older principle under my objection, one I learned in permaculture and have never found reason to drop: surplus returns to the system that produced it. A healthy system cycles its surplus back to keep the whole thing alive. The cap is where we let the surplus pool and sit. Scrapping it returns the harvest to the ground that grew it.

So here’s the correction, plainly.

Scrap the cap. The same rate on every dollar of wage income, first to last. The janitor already pays 6.2 percent on everything he earns. The executive can do the same. No ceiling, no seam, no door at $184,500 where the duty to everyone else ends.

Push the retirement age down, and keep pushing it. Start by reverting the minimum to 55 and full retirement to 62. Then keep lowering it as the math allows, because the math has moved. We are far more productive than the country that set retirement at 65, then 67. With the technology already in our hands, a working life of roughly 22 to 50 is within reach — you give the economy your strong decades and you get the rest of your life back. A high retirement age is its own hidden transfer, too: the people who do the body-breaking work tend to die sooner, so they pay in the longest and collect the least, while the desk class lives longer and draws longer. Bring the age down and “retire healthy” stops being a slogan. It means getting out with years and a working body still in front of you.

Pay by work, not by income. Here’s where the merit lives, so let me be clear about it. You earn your benefit by working. Quarters worked, credits earned, counted the same way the system already counts them. You put in to draw out — that requirement stays exactly where it is. What changes is the formula for what you draw: the rate, times the quarters you worked, times the age you retire. Income while working never enters it. Two people who put in the same quarters and retire the same year draw the same check, whether one ran the hospital and the other mopped its floors. Both had to work to get there, year after year, paying in. That’s the merit, and we keep all of it. We strip out only the part that scaled your retirement to your old paycheck, because a floor should sit at the same height for everyone standing on it.

A word on disability, which I’m keeping separate on purpose. There are systems for it now, measured through SSI, and there will be systemic adjustments to make. That’s a real and serious issue, and it earns a direct treatment on its own terms instead of getting folded in here to muddy both arguments. This column is about the retirement side. The disability side gets its own.

The surplus the cap shelters at the top is what funds the earlier age and the level floor at the bottom. That’s the trade, and it’s honest. I’ll name what it changes: today the system pays you back roughly in proportion to what you earned. We’d replace that with a flat floor everyone stands on equally. That’s the point of the design.

“A rising tide lifts all boats” has always carried a little dishonesty, because the water was never the same depth under everyone. Some boats sat in a harbor that filled. Others sat on mud. Here’s how the saying comes true: one rate in, one floor out, the age coming down as our productivity climbs, and an end to the seam that hands the wealthy a private door into the capital economy untaxed. Retire healthy, early enough that your body is still your own. Retire wealthy — secure, on a floor that doesn’t flinch at the difference between a surgeon and a steelworker. Build that, and you’ve made late-life universal income out of a system the country already funds and already trusts. The cap comes off, the age comes down, the floor goes level, and the tide rises — all of it, together.